“Medicare enrollees regret not revisiting their plan’s drug coverage yearly. They don’t realize that drug manufacturers can change their prices annually which can trigger changes in their plan’s Prescription Drug Coverage. For example, a medication you take might move from tier one to tier three, with a much higher deductible. It’s super important to revisit your plan’s prescription drug coverage during the Annual Enrollment period.” That’s the first of Kimberly Homes’ invaluable hints for avoiding Medicare regrets in this article. Read on for six more!

Agent Kimberly Homes deals exclusively with Medicare policies and ancillary products to complement Medicare supplements.

Homes is an independent insurance agent who deals exclusively with Medicare policies. What do people wish they had known…wish someone had told them…or regret not having considered more thoughtfully when it comes to Medicare? We asked Homes and she started by contrasting the private insurance we’re all familiar with and Medicare.

“Group health insurance provides identical coverage for everyone in the group, regardless of need. Medicare is individualized. Spouses who may have been insured on the same policy through an employer often choose different Medicare plans that better address their differing needs.”

Medicare’s Basic Components

Part A (hospital insurance) typically does not have an out-of-pocket premium but does have deductibles and coinsurance.

Part B (doctor visits, Emergency Room, tests, ambulance) has a monthly premium of $174 in 2024 for individuals whose income is less than $103,000 ($206,000 for couples filing taxes jointly). Higher incomes incur higher monthly premiums.

Part D (prescription drug coverage) In 2024, the national base premium is $34.70 per month, (subject to the same income limits as part B) but premiums can vary by plan. Deductibles can vary by plan as well, but Medicare caps a medication’s deductible at $545.

Medigap Plans

A very small percentage of the Medicare population chooses Parts A + B + D only. More often, Medicare enrollees also select a Medigap (supplemental) policy such as Parts F, G, or N to fill in gaps in Part A and Part B coverage. Premiums and coverage vary by plan.

Homes’ Hint: “The only difference between 2 insurance companies’ Medigap policies is the price. For example, Plan G’s coverage is the same, no matter what company you choose.”

Medicare Advantage Plans

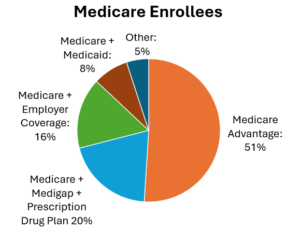

Medicare Advantage plans are chosen by more than half of all Medicare enrollees. They combine Part A and Part B (though you still need to pay the Part B premium) and most include prescription drug coverage. Many Advantage plans offer limited coverage for vision, dental, and hearing. Some add reimbursements for over-the-counter drugs and fitness memberships. Most Advantage plans have a network of participating providers, and pre-approval from the plan plus a referral from your primary care physician may be required for specialists’ services. Premiums and coverage vary by plan.

Homes’ Hint: “Prescription drug prices, relative to each plan, usually drive what Advantage plan or what Personal Drug Plan (PDP) is best for you.” (Related – 1 in 2 seniors fail to take medications as prescribed.)

Data: KFF, an independent source of health policy research, polling, and journalism.

Homes said, “Everybody asks, ‘Do I have to sign up for Medicare?’ The answer is “No” if you have what the government calls creditable coverage – coverage that’s expected to pay, on average, at least as much as Medicare drug coverage. This could be through a current or former employer or union, or individual health insurance, for example. If you are still working and have group coverage that is considered creditable coverage you do not have to sign up for Medicare until you are ready to retire.”

Homes’ Hints: Cobra and Affordable Care Act/Marketplace policies are not considered creditable coverage.”

Choosing the Right Medicare Coverage

This is essential for avoiding Medicare regrets. According to Homes, “Some group insurance policies are better than Medicare, and vice versa. There’s a lot to compare in terms of coverages, cost, provider access, and out-of-pocket maximums. There is no one best policy for everybody. Everybody’s healthcare needs are different.”

Medigap or Advantage? This is a common question Homes receives. She explained that Medigap policies appeal more to people seeking the widest variety of providers – anyone who accepts Medicare – and without the need for prior approval. According to the Commonwealth Fund, the top 2 reasons people chose a Medicare Advantage plan are: the expanded benefits their plan offers (24%); and the plan’s cap on out-of-pocket expenses (20%).

Homes’ Hint: Medigap plans do not include a drug plan. You also enroll in a Part D Prescription Drug Plan through Medicare at the time of enrollment or face a lifetime late enrollment penalty when you sign up later.

An Agent’s Role

While people can sign up for Medicare on their own, making the best coverage/policy decision requires extensive research and learning. Homes said, “People need to talk to someone who understands the rules and can guide them. Agents provide Medicare education for free. Whatever plan you sign up for, it doesn’t cost more.”

Homes’ Hint: “People should start their search early and get educated about Medicare.”

Homes went on to explain one of her most important roles is helping her clients compare their options. Prescription drugs are assigned a tier (preferred generic, generic, preferred brand name, etc.) and then there are phases throughout the year, during which the price you pay for your prescriptions changes. She explained that she enters all of a client’s prescriptions into a computer program that looks at those Rx costs to help identify what is the best coverage/policy. Her goal is to determine the most economical way to pay for their drugs. For individuals that can’t afford a specific medication, Homes helps them fill out a “patient assistance” application which their doctor has to sign, and they may be able to receive their medication at a reduced price (income limits apply.) “This is my favorite part of Medicare. It’s almost like solving a story problem.” Homes stated.

Homes also distinguished the two types of agents. “Captive agents represent a single insurance company and offer that company’s Medicare policies. Independent agents represent lots of insurance companies and can help compare and identify the best policy for the client.”

Enrollment

Homes said people wish they had better understood that they cannot sign up for Medicare whenever they want. “There are specific enrollment periods, depending on your situation.”

Initial Election Period: 3 months before, the month of, and 3 months after your 65th birthday.

Annual Election Period: October 15th – December 7th of every year.

Open Election Period: January 1st through March 31st. Limited to Medicare Advantage plans and only for individuals currently enrolled in an Advantage plan.

Special Election Period: (Specific to the individual for situations such as: loss of employer coverage or change of residence.)

Homes’ Hint: “Once you sign up for Medicare, you cannot contribute to your Health Savings Account.”

Switching plans

Finally, Homes advised that many people don’t understand the rules for switching Medicare plans, another aspect of avoiding Medicare regrets.

If you have Medigap:

- You can switch to another Medigap plan if you are looking for a lower premium any month of the year. You just need to pass medical underwriting.

- You can only switch to an Advantage plan only during the Annual Election Period (October 15 – Dec. 7.)

Prescription Drug Plans:

- You can change prescription drug plans between October 15 and December 7.

If you have an Advantage plan:

- You can switch to another Advantage plan between October 15 and December 7. You can also switch between January 1 and March 31.

- If you have an Advantage plan, you can switch to a Medigap plan anytime during the first 12 months of having an Advantage plan. This is called a trial right.

- If you start Medicare with an Advantage plan and you delayed your Part B, your 12-month trial right to switch to a Medigap plan is determined by your Part A effective date. Therefore, you may have to go through medical underwriting to switch to a Medigap plan.

Homes summarized, “There are so many rules and nuances with Medicare it would be easy to miss something.” We agree! While Medicare does not pay for Sunlight Senior Care’s non-medical in-home care services, Medicare is the bedrock of our clients’ health care and we’re pleased that we might be able to help in terms of avoiding Medicare regrets. We are grateful for individuals like Kimberly Homes who have also chosen to serve seniors and assist them in making wise, informed decisions.

Our thanks to Kimberly for sharing her insights on avoiding Medicare regrets by getting the right Medicare policy. Homes, based in Wahoo, NE, caters to clients in Lincoln, Omaha and the surrounding area. She can be reached at (402) 429-1311.